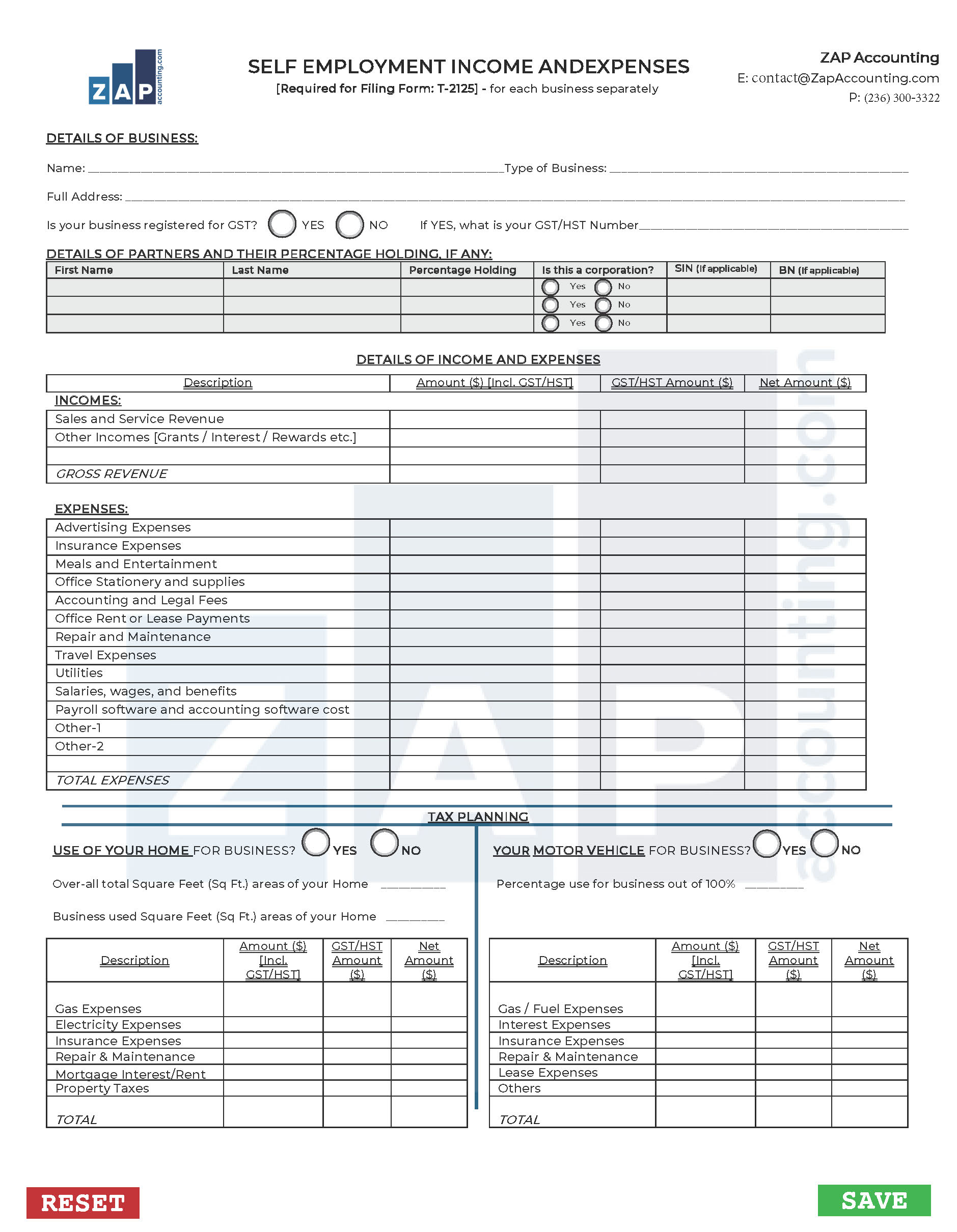

Form T2125: A Guide for Canadian Self-Employed Individuals

If you are self-employed in Canada, Form T2125 – Statement of Business or Professional Activities is a crucial document for reporting your business income and expenses to the Canada Revenue Agency (CRA). Whether you’re a freelancer, consultant, contractor, or small business owner, filing this form correctly can help you maximize deductions and ensure compliance with tax laws.

What is Form T2125?

Form T2125 is used by individuals to report income and expenses related to:

- Business activities (sole proprietors and partnerships)

- Professional activities (lawyers, doctors, accountants, etc.)

- Commission income (for those who earn commissions but are not employees)

Who Needs to File Form T2125?

You must file this form if:

✔ You are self-employed (full-time or part-time).

✔ You run a business as a sole proprietor or a partnership.

✔ You provide professional services.

✔ You earn income from commissions outside of employment.

Key Sections of Form T2125

1. Business Identification

- Business name and address

- Industry code (specific to your business sector)

- Business number (if registered)

2. Income Statement

- Gross sales, commissions, or fees

- Returns and allowances

- Total business income

3. Expense Deduction Categories

Self-employed individuals can claim various expenses to reduce taxable income. Some key deductible expenses include:

- Office expenses: Supplies, postage, stationery, etc.

- Home office expenses: Rent, utilities, property taxes (based on usage percentage).

- Vehicle expenses: Gas, insurance, repairs, and depreciation (if used for business).

- Advertising & marketing: Website costs, ads, and promotions.

- Professional fees: Accounting, legal, and consulting services.

- Business travel: Hotel, flights, and meals (subject to 50% limit).

- Depreciation (CCA – Capital Cost Allowance): Claim for business assets like computers, vehicles, and furniture.

4. Calculation of Net Business Income

- Total expenses are subtracted from total business income to determine net income.

- This amount is transferred to line 13500 of your T1 General tax return.

Case Studies: Real-Life Scenarios

Case Study 1: Sarah – Digital Marketing Freelancer

Background

Sarah is a self-employed digital marketing consultant based in Toronto. She earns $85,000 annually from her freelancing work. She operates from her home office and incurs various expenses related to running her business.

Business Expenses & Deductions

| Expense Type | Amount Spent | Eligible Deduction | Calculation Details |

|---|---|---|---|

| Home Office | $30,000 (annual home cost) | $3,000 | 10% of home used for business ($30,000 × 10%) |

| Internet & Phone | $2,400 | $1,200 | 50% business use ($2,400 × 50%) |

| Advertising | $6,500 | $6,500 | Fully deductible |

| Office Supplies | $1,200 | $1,200 | Paper, printer ink, notebooks, etc. |

| Laptop (CCA – Class 50) | $2,500 | $1,500 | 55% depreciation in the first year |

| Professional Fees | $1,500 | $1,500 | Accounting & consulting fees |

| Business Meals | $1,000 | $500 | 50% of eligible meals deductible |

Detailed Explanation of Expense Claims

1. Home Office Expenses

Sarah uses 10% of her home exclusively for work. The CRA allows her to deduct a proportionate amount of expenses like:

- Rent or mortgage interest

- Property taxes

- Utilities (electricity, water, heating, internet, home insurance, etc.)

- Maintenance (repairs related to office space only, e.g., painting the office room)

📌 Formula:

Total Home Expenses × % of Home Used for Business

✅ Claimed Amount:

$30,000 × 10% = $3,000 deduction

2. Internet & Phone Expenses

Sarah uses her internet and phone for both personal and business purposes. CRA allows only the business portion to be claimed.

✅ Claimed Amount:

$2,400 × 50% = $1,200 deduction

3. Laptop (Capital Cost Allowance – CCA Class 50)

- A laptop/computer is a capital asset, meaning it cannot be fully deducted in the year of purchase.

- Instead, it qualifies for CCA (Capital Cost Allowance) under Class 50 (55% depreciation in year one).

✅ Claimed Amount:

$2,500 × 55% = $1,500 depreciation deduction in year one

Case Study 2: John – Self-Employed Electrician Using a Work Vehicle

Background

John is a self-employed electrician earning $95,000 per year. He uses his truck for business purposes, including traveling to client sites, purchasing supplies, and hauling tools.

Business Expenses & Deductions

| Expense Type | Amount Spent | Eligible Deduction | Calculation Details |

|---|---|---|---|

| Fuel | $5,000 | $3,500 | 70% business use ($5,000 × 70%) |

| Maintenance | $2,500 | $1,750 | 70% business use ($2,500 × 70%) |

| Insurance | $1,800 | $1,260 | 70% business use ($1,800 × 70%) |

| Vehicle CCA (Class 10 – 30%) | $30,000 (truck cost) | $9,000 | 30% depreciation in the first year |

| Parking & Tolls | $800 | $800 | Fully deductible for business-related travel |

Detailed Explanation of Expense Claims

1. Vehicle Expenses (Fuel, Maintenance, Insurance, Parking, CCA, etc.)

John uses his truck 70% for business, meaning he can claim only 70% of fuel, repairs, and insurance.

📌 Formula:

Total Vehicle Expense × % Business Use

✅ Claimed Amounts:

- Fuel: $5,000 × 70% = $3,500

- Maintenance: $2,500 × 70% = $1,750

- Insurance: $1,800 × 70% = $1,260

- Parking & Tolls: Fully deductible (only for business travel)

2. Vehicle Capital Cost Allowance (CCA – Class 10: 30%)

- Vehicles fall under Class 10, allowing a 30% CCA claim in the first year.

- John purchased a truck for $30,000, so he can claim $9,000 in depreciation.

✅ Claimed Amount:

$30,000 × 30% = $9,000 depreciation deduction in year one

Case Study 3: Rachel – Real Estate Agent (Commission-Based Income)

Background

Rachel is a real estate agent earning $120,000 per year. She incurs several expenses, including marketing, car expenses, and office costs.

Business Expenses & Deductions

| Expense Type | Amount Spent | Eligible Deduction | Calculation Details |

|---|---|---|---|

| Car Lease | $7,200 | $3,600 | Max 50% deductible ($7,200 × 50%) |

| Fuel & Maintenance | $6,000 | $3,000 | 50% business use |

| Advertising & Signs | $10,000 | $10,000 | Fully deductible |

| Business Travel | $5,000 | $2,500 | 50% of meals & entertainment |

Special Expense Rules for Commission-Based Employees (Real Estate, Sales, etc.)

- Car Lease Limitation: CRA allows only 50% of car lease payments to be deducted.

- Business Meals: 50% deductible when meeting clients.

- Travel Costs: If related to business, flights, hotels, and meals can be claimed (subject to CRA limits).

✅ Total Deductions Claimed: $19,100

Key Takeaways on Claiming Expenses from Form T2125

✅ Keep Proper Records:

- Maintain receipts, invoices, and mileage logs.

✅ Only Claim the Business Portion:

- Expenses used partially for business must be pro-rated (e.g., home office, vehicle, phone).

✅ Understand CCA Rules:

- Capital assets like vehicles, laptops, and office furniture must be depreciated over time.

✅ Know CRA Limits:

- Meals (50%), vehicle lease (50%), and home office (only business portion) have deduction caps.

Final Thoughts

Form T2125 can significantly reduce your taxable income if you track and claim expenses correctly. Whether you’re a freelancer, contractor, or commission-based worker, understanding these tax rules can save you thousands each year.

Need Help? Contact ZAP Accounting!

Filing Form T2125 correctly can help you maximize deductions and reduce your taxable income. If you need expert advice on claiming business expenses, ZAP Accounting is here to assist! Contact us at +1 236 300 3322 for professional guidance on filing your self-employment taxes.

Form T2125 – Self-Employed Business Income & Expense Worksheet: Download, Print, Fill and Submit

{kind=link}

Disclaimer

This article provides general information about child care expenses based on current tax laws. Tax regulations are subject to change, and this article may not reflect the latest updates. The information provided may contain errors or omissions. Before making any tax-related decisions, please consult the CRA website or seek professional advice from a ZAP Accounting expert to ensure accuracy and compliance.